Global growth outlook for 2026

The macroeconomic baseline for 2026 is defined by a widening divergence between the United States and the rest of the world. While global expansion remains positive, the pace of growth is moderating, creating a landscape where regional resilience varies significantly. This split is not merely statistical; it reflects differing monetary trajectories, fiscal constraints, and structural demand shifts across major economies.

Goldman Sachs Research projects global GDP growth of 2.8% in 2026, a figure that outpaces the broader consensus forecast of 2.5%. Their analysis highlights that the United States will likely outperform substantially, driven by sustained consumer spending and resilient labor markets. This US strength stands in contrast to softer activity in Europe and parts of Asia, where industrial output and household consumption face headwinds from higher borrowing costs and weaker external demand.

Morgan Stanley offers a slightly more optimistic baseline, forecasting global real GDP growth at 3.2% for 2026, up from approximately 3.5% in 2025 before settling into a slower trajectory. Their outlook suggests that while the global economy avoids a sharp downturn, the era of synchronized expansion is over. Investors must therefore navigate a fragmented environment where US assets may continue to show relative strength while international markets adjust to lower-growth realities.

Equity earnings and sector rotation

The 2026 equity landscape is defined by a widening divergence in corporate earnings power, with the United States maintaining a distinct advantage over international markets. Analysts at State Street project US stock earnings to grow by 13.5 percent this year, significantly outpacing the 8.7 percent growth forecast for Europe, Australasia, and the Far East (EAFE) indices [src-serp-3]. This disparity underscores the resilience of the American corporate sector, largely driven by capital expenditure in artificial intelligence and technology infrastructure.

The AI-driven bull market remains the primary engine for this growth, with soaring earnings and sustained spending fueling continued momentum [src-serp-4]. However, this concentration of growth in specific sectors introduces valuation risks that warrant close monitoring. As technology stocks extend their rallies, investors must weigh the strength of underlying earnings against potential overvaluation, especially as broader macroeconomic factors like interest rates and inflation remain in play.

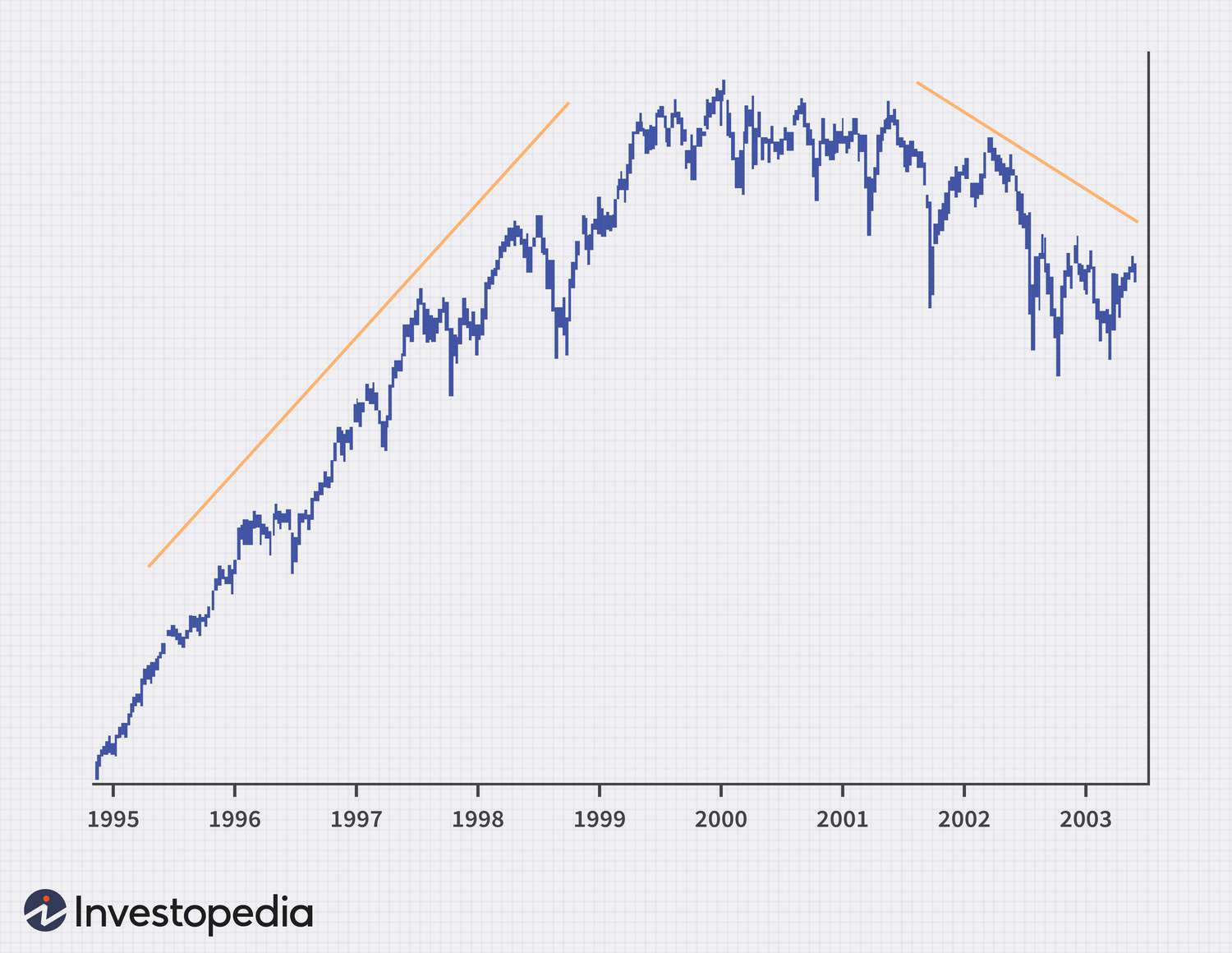

To visualize the trend momentum of the technology sector, which is central to this earnings narrative, we look at the performance of the Technology Select Sector SPDR Fund (XLK). This chart illustrates the recent price action and volume trends that reflect the market's confidence in AI-driven growth.

Energy supply and inflation risks

The global oil market is navigating a paradoxical landscape in 2026. While overall supply is forecast to outstrip demand growth, the margins are dangerously tight. This structural imbalance creates a fragile environment where minor disruptions can trigger disproportionate price spikes, feeding directly into broader inflationary pressures.

JPMorgan Global Research projects world oil demand will expand by 0.9 million barrels per day (mbd) in 2026, rising to 1.2 mbd in 2027. Despite this steady growth, the supply side is not keeping pace with the ease of previous years. The market is operating with limited spare capacity, meaning that any geopolitical tension or production cut can quickly tighten the buffer.

This fragility poses a direct threat to central bank policy. An extended oil crunch does not just raise consumer costs; it complicates the path to lower interest rates. As Fidelity Investments notes, soaring energy costs can reignite inflation, forcing monetary authorities to maintain higher rates for longer than markets currently expect.

The uncertainty is compounded by the lack of transparent, real-time data on global inventories and production quotas. Investors are left navigating a market where the fundamental supply-demand equation is shifting underfoot. This environment favors those who can quickly assess supply shocks and their inflationary implications.

The interplay between oil prices and inflation expectations is no longer a secondary concern; it is a central driver of asset allocation. As energy costs fluctuate, the risk of stagflationary pressures increases, challenging the traditional correlation between growth and inflation. Markets must price in the possibility that energy volatility will remain a persistent headwind for global growth.

Real estate and labor market softening

The equity bull market faces a counterweight in the slowing U.S. economy. CBRE’s 2026 outlook projects annual GDP growth to decelerate to 2.0%, driven by softening labor conditions and marginally lower inflation. This economic cooling is not uniform; it is most visible in sectors sensitive to borrowing costs, particularly real estate.

Higher interest rates have dampened demand for commercial and residential properties, leading to increased vacancy rates and slower price appreciation. The labor market, once a pillar of economic resilience, is showing signs of strain as hiring slows across key industries. This softening suggests that the recent strength in consumer spending may not be sustainable without further wage growth.

Investors should view these trends as a signal to diversify away from rate-sensitive assets. The disconnect between equity valuations and underlying economic fundamentals is widening, creating potential headwinds for growth stocks that rely on future earnings expectations.

Strategic positioning for 2026

Use this section to make the Market Trends decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

No comments yet. Be the first to share your thoughts!